Mortgage rates remain one of the hottest topics in today’s housing market—and for good reason. Following a weaker-than-expected jobs report, the bond market responded almost immediately, pushing mortgage rates down to 6.55% in early August—the lowest level we’ve seen so far this year.

At first glance, that dip may not seem dramatic. But for many buyers who have been holding out for a break, even a modest decline sparks fresh optimism that rates could finally be heading lower. The big question is: how much of a shift can we really expect moving forward?

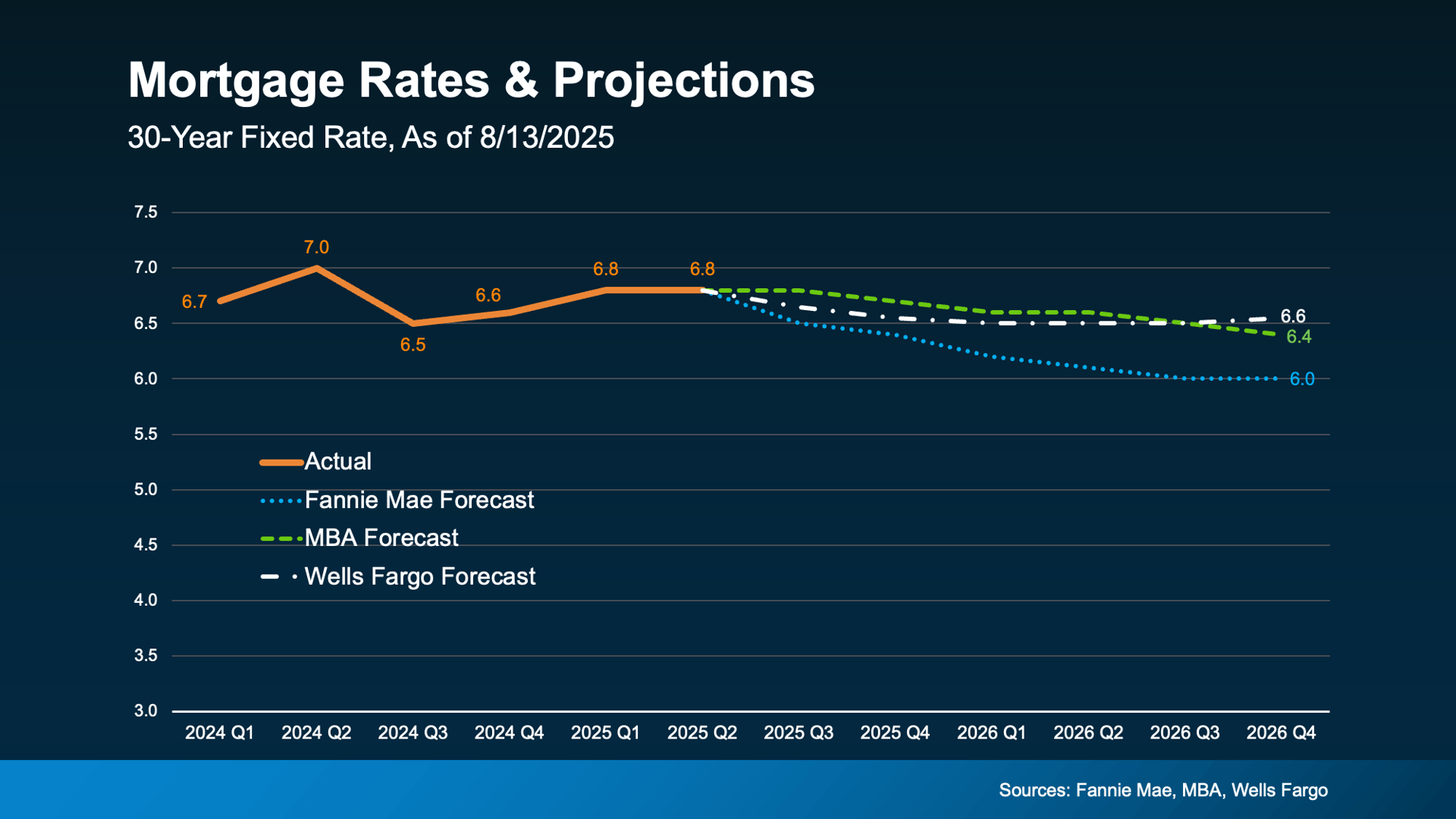

What’s Next for Mortgage Rates?

Big shifts in mortgage rates aren’t expected anytime soon—but smaller moves, like the recent dip we just saw, are still likely. Each time new economic data comes out, rates can adjust. And with several reports on the horizon, we’ll soon have a clearer picture of where the economy and inflation are heading, and how mortgage rates might respond.

The Rate Buyers Are Waiting For

The number most buyers are watching closely is 6%. It’s not just a nice round figure—it makes a real difference in affordability. According to the National Association of Realtors (NAR), if rates reach 6%:

-

5.5 million more households could afford the median-priced home

-

Roughly 550,000 buyers would enter the market within 12 to 18 months

That’s a lot of pent-up demand waiting to jump in. And with forecasts from Fannie Mae suggesting we could see that milestone next year, it raises the big question: is it worth waiting?

The Tradeoff of Waiting

Here’s the catch—if you’re waiting for 6%, you’re not the only one. Once rates drop further, more buyers will re-enter the market, which means:

-

More competition

-

Fewer options

-

Higher prices

NAR puts it simply: “Home buyers wishing for lower mortgage interest rates may eventually get their wish, but for now, they’ll have to decide whether it’s better to wait or jump into the market.”

Why Now Could Be Your Window

Right now, conditions are actually in buyers’ favor:

-

Inventory is higher → more choices

-

Price growth has cooled → more realistic pricing

-

Negotiation is possible → better deals today

These advantages may not last if rates fall and demand surges again. As NAR notes: “Buyers who are holding out for lower mortgage rates may be missing a key opening in the market.”

Bottom Line

Rates probably won’t hit 6% this year. But when they do, you’ll likely face more competition and less flexibility. If you’d rather buy with less pressure and more negotiating power, that opportunity may be here now.

Talk with a local real estate professional to see how conditions in your area stack up—and whether moving sooner could be your best move.